At the 2025 Ben Graham Conference, the International Value Investments panel explored whether global value stocks are finally poised to outperform. Moderator Henry Mallari-D’Auria, CIO of Global & Emerging Markets Equities at Ariel Investments, led the discussion with panelists including Matthew Fine, Portfolio Manager at Third Avenue Management; Christian Heck, Portfolio Manager at First Eagle Investments; Amelia Koh, Analyst at Tweedy, Browne; Krishna Mohanraj, Portfolio Manager for International Strategy at Diamond Hill; and Waldemar Mozes, Director of Investments at Cedar Street Asset Management. Together, they examined value selection, non-U.S. opportunities, and the disciplined frameworks guiding their global portfolios.

At the 2025 Ben Graham Conference, the International Value Investments panel explored whether global value stocks are finally poised to outperform. Moderator Henry Mallari-D’Auria, CIO of Global & Emerging Markets Equities at Ariel Investments, led the discussion with panelists including Matthew Fine, Portfolio Manager at Third Avenue Management; Christian Heck, Portfolio Manager at First Eagle Investments; Amelia Koh, Analyst at Tweedy, Browne; Krishna Mohanraj, Portfolio Manager for International Strategy at Diamond Hill; and Waldemar Mozes, Director of Investments at Cedar Street Asset Management. Together, they examined value selection, non-U.S. opportunities, and the disciplined frameworks guiding their global portfolios.

Also our coverage of the 2025 Sohn Monaco Conference, 2025 Global Alts New York and the Best Alternative Investment Fund Conferences for 2025.

2025 Ben Graham Conference – Matthew Fine, Christian Heck, Amelia Koh, Krishna Mohanraj, and Waldemar Mozes

Moderator’s Opening Remarks & Panelist Introductions

The moderator, Henry Mallari-D’Auria, opened the panel by stating, “This is the panel you have waited for, perhaps for a decade. What’s going to happen outside the United States? Will it finally perform? The case for attractive valuation has been there for a while, but will value perform? Have we already started to see the change in direction in non-US equities? That’s what you are here to find out, and we are thrilled with a great panel to help us out”.

He explained the initial format: “Over the next few minutes, each of our panelists will give some answers, but I think what we’ll start with is letting them each describe who they are, what their philosophy and firm represent, and give us an example of an investment they’ve made that highlights the way they invest. If they each take roughly three or so minutes, that will leave us time to get into more robust questions”.

Panelist Firm Philosophies & Investment Examples

Matthew Fine, Third Avenue Management

Matthew Fine noted that Third Avenue was founded by legendary value investor Marty Whitman in 1986. Their core strategy for all funds is to buy at a cheap valuation, which derives from investor pessimism, making it contrarian at the time of investment. The key is to buy when the market is “cloudy” but wait 3-5 years for conditions to improve.

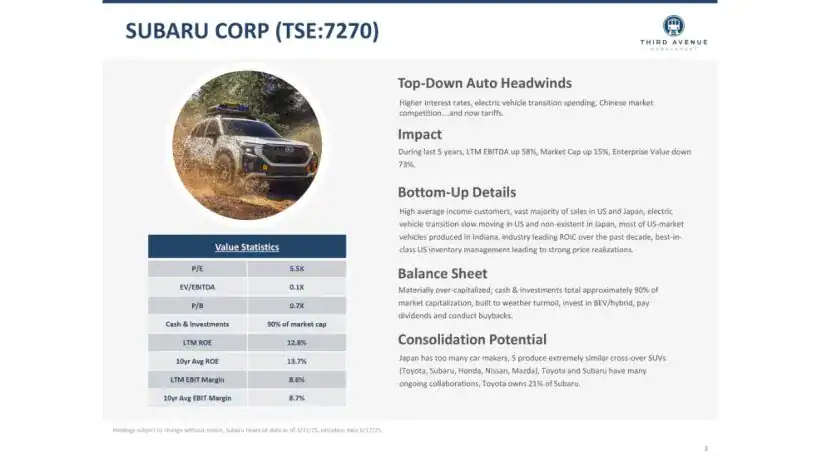

Investment Example: Global Automotive Industry

- Matt highlights the global automotive industry as an example of a “cloudy” investment.

- The sector currently shows valuations around 5.5x Price-to-Earnings (PE) and almost zero on Enterprise Value-to-EBITDA, with 90% of market capitalization held in cash.

- This valuation is due to investor pessimism around factors like tariffs and China’s entry into the market.

- Despite these concerns, the industry’s EBIT (Earnings Before Interest and Taxes) margin is strong for the sector, and their exposure is primarily in the US and Japan with low China influence.

Christian Heck, First Eagle Investments

Christian Heck, originally from Germany, described First Eagle Investments, noting their history dates back to the 1870s and they manage approximately $150 billion today. Their value fund was incepted 46 years ago and was run by Jean-Marie Eveillard, who had a close relationship with Marty Whitman. First Eagle has compounded about 13% annually since inception over those 46 years. They are “global, go anywhere” value investors, focusing on price and a margin of safety.

Investment Example: Get Tencent At A Discount

- This stock is the investment holding of two South African entrepreneurs who made a significant investment in 2001 into the Chinese tech company, Tencent.

- Tencent has been one of the greatest investments of all time, compounding at about 40% annualized.

- The stock owns about 25% of Tencent, which is its main asset.

- Tencent operates WeChat, an app with 1.4 billion users in China who spend close to two hours daily using it for communication, payments, social media, and video.

- Tencent has grown its top-line revenue and operating income by over 20% annualized in the last decade.

- First Eagle was historically skeptical of China investments but saw a great opportunity during the property bubble burst and tech crackdown.

- Tencent was trading at attractive multiples (e.g., 13.5x operating income), but buying through the stock (Prosus) offered an even deeper discount, a “double discount,” of about 30% off.

- Prosus is listed in the Netherlands for tax efficiency.

- A key driver of returns is Prosus’s open-ended share buyback program, having retired about 35% of outstanding shares over the last three years.

Amelia Koh, Tweedy, Browne

Amelia Koh stated that Tweedy, Browne was involved in market making in 1920 and began managing money in 1959 using a Ben Graham style. Their flagship fund holds about 90 stocks, and 40% of their fund is invested in small- and mid-cap stocks. They are generally longer-term shareholders, looking at investments in terms of years and months.

Investment Example: Computacenter plc (LON:CCC)

- ComputaCenter (CCC) is an IT software reseller operating in eight markets, including the UK, US, and Germany.

- Germany alone represents about half of its revenue.

- The company has a good track record and operates in a fragmented industry with high returns to shareholders.

- It maintains a net cash balance sheet.

- Tweedy, Browne purchased the company at about 8x EBITDA when it was experiencing a temporary slowdown in 2024 due to the digitization of demand and cost impacts of the pandemic, along with other minor factors. They believe this slowdown is not structural and that ComputaCenter, as a German company, will benefit from increased government spending and German stimulus.

Krishna Mohanraj, Diamond Hill

Krishna Mohanraj manages the international team at Diamond Hill, a firm with $30 billion in assets under management that focuses entirely outside the US. Their team of five senior analysts focuses exclusively on non-US markets, covering all geographies. They are a “very focused team,” spending most of their time understanding management teams and market landscapes by talking to them directly.

Investment Example: Allied Irish Bank Group plc (LON:AIBG)

- Diamond Hill invested in the Irish banking market, which is highly consolidated. Three banks hold about 90% market share, with Allied Irish Bank having about 33%.

- The market structure makes it interesting because retail banking is a commoditized business where scalability provides a significant advantage and pricing power.

- Ireland’s economy is strong, based on knowledge, and its regulator is very pro-consolidation, making it difficult for outsiders to enter the market.

- The Irish government is slowly reducing its stake in banks, which also presents an improving macro setup.

- Allied Irish Bank had a return on equity of 90% for the year against a target of 14-15%, with a capital return target of 50% market cap. They project shareholders could receive 30% of market value back over the next three years.

Waldemar Mozes, Cedar Street Asset Management

Waldemar Mozes, originally from Transylvania, founded Cedar Street Asset Management in Chicago in 2016. The firm has $650 million in assets under management across three strategies, focusing on non-US small cap investing. They are contrarian and pure-play non-US small cap focused, recognizing that while markets are efficient long-term, they are less efficient short-term. Their investment philosophy centers on quality businesses with strong balance sheets and operating performance that are currently underappreciated by the market due to dynamic factors in their geography or business climate.

Investment Example: Glanbia plc (LON:GLB)

- Glanbia is a global nutrition company that is one of the biggest providers of cheese in the US.

- It has about a $4 billion market cap and $4 billion in sales, with 70% of its business in the US.

- Glanbia operates three businesses: performance nutrition, an ingredients business, and wholesale cheese.

- The stock came under pressure due to short-term dynamics around whey pricing and sentiment regarding performance nutrition brands (like SlimFast) due to GLP-1 products.

- However, Waldemar believes these are short-term dynamics, and the performance nutrition market is actually growing, partly because GLP-1 is causing people to focus more efficiently on protein and other nutrition, leading to very nice growth for Glanbia.

- The performance nutrition business grows 7-8% annually with 15-20% EBITDA margins, while the wholesale cheese business grows at a slower rate.

- The market often struggles to value such combined “good” and “bad” businesses.

- Cedar Street believes value can be unlocked by spinning off one or both sides of the business. Activists have recently promoted this idea to Glanbia’s primary shareholders, the Irish dairy cooperatives. Waldemar believes value will likely increase over time, whether through market recognition or activist pressure.

Building an International Portfolio: Opportunities & Risks

The moderator then posed a question to the panel: “How would you think about both the opportunities when you build an international portfolio, considering sectors, countries that you want exposure to, as well as the risks? What are you trying to avoid when you’re building a portfolio outside the US today?”.

Matthew Fine: Focus on Cheapness and Economic Returns

He looks for cheapness, thinking like a business owner: “Where can I in the world go buy a business that will generate absolute economic returns to me as an owner of that business, that will provide satisfactory return?”. He is willing to invest almost anywhere.

His global strategy currently has only 13% weight in the United States, which is very low compared to benchmarks like the MSCI World. He has found it “terrific struggle” to find attractive value in the US.

He is concerned about risks such as currency risk, currency mismatches, leveraged companies, political risk, and control party risk. His strategy is paramount to investing in “super well-financed companies”.

Christian Heck: Scarcity and Diversification

First Eagle looks for businesses with scarcity, which can be intangible (e.g., intellectual property, strong brand lock) or tangible (e.g., unique geological assets).

Examples include Shimano (controlling 70-80% of bicycle brakes) and Grupo Mexico (owning rail networks and copper mines in Mexico).

They are diversified and long-term investors, believing the best approach is to own a portfolio of reasonably valued assets.

They look for a 30% margin of safety compared to what an owner would pay.

Krishna Mohanraj: Disciplined “No” and Balance Sheets

He emphasizes saying “no” to many opportunities, given their focused portfolio of 35-55 stocks. They ask if a company is “attractive enough to make it past that 40 stock cutoff” to be long-term owners.

Understanding the balance sheet is more important than valuation for them.

They prefer local banks over large, complex banks for this reason.

Many reasons for rejection include business quality, capital allocation history, potential government interference, or simply being too complex to understand (e.g., Chinese real estate).

Waldemar Mozes: Active Approach due to Governance Issues

Waldemar stresses that international investing is not as simple as US investing due to the “biggest overlooking element” being corporate governance issues.

Investors deal with multiple jurisdictions, securities regulators, banking schemes, and macro dynamics (like interest rates), all impacting the portfolio.

Therefore, they strongly advocate for an active approach rather than passive vehicles like ETFs, which don’t weed out “low garbage”.

Specific Investment Strategies & Considerations

Gold as a Hedge

Christian Heck explained that First Eagle is “first and foremost concerned for protection,” and has historically held gold as a hedge. While money supply grows several percent per year, gold supply only grows about 1% annually, making it a good long-term hedge. Gold has historically shown uncorrelated returns to stocks and yields high single digits. They consider a 10% allocation to gold a good number for hedging, preferring it over strategies like CDS that incur premiums.

Non-US Small Caps (Cedar Street)

Waldemar Mozes highlighted that non-US small caps tend to outperform large caps by a wide margin historically. Investors often don’t realize that not only are returns better, but volatility is roughly the same, leading to outperformance on a risk-adjusted basis. Non-US small caps also exhibit lower correlation compared to non-US large-cap stocks and a higher Sharpe ratio, making them a valuable inclusion in a portfolio.

Activist Approach

Amelia Koh clarified that Tweedy, Browne is not a traditional activist but will sometimes engage in such efforts. She cited the example of Winpak, where a colleague advocated for share buybacks given the company’s strong cash position and trading below market value. Winpak subsequently launched a successful share buyback program.

Rapid-Fire Questions

The moderator then asked for one thing each panelist thought was misunderstood about international investing.

Matthew Fine: The magnitude of the valuation difference between US and international markets, noting US valuations are roughly twice that of the rest of the world today. He also highlighted Japanese semiconductor companies as critical suppliers for advanced equipment like ASML, a fact often unappreciated.

Christian Heck: The idea that the US has a monopoly on great, dominant companies.

Amelia Koh: How cheap international markets are on an absolute basis.

Krishna Mohanraj: The number of quality companies available internationally.

Waldemar Mozes: The actual riskiness of international investing, suggesting it’s often perceived as riskier than it is.

When asked about their favorite value investor/icon:

Matthew Fine: Besides Marty Whitman, his hero was Sam Zell. He had memorable experiences meeting and doing research with him.

Christian Heck: Warren Buffett, admiring his personality and humility.

Amelia Koh: Warren Buffett.

Krishna Mohanraj: Humility.

Waldemar Mozes: Charlie Munger.

Audience Q&A

Q: Where Will the Buyers Come From for Non-US Value Stocks?

An audience member, Kendrick Kilmer, questioned where buyers would come from for non-US value sets, given the scrutiny value investors face.

Waldemar Mozes: Cited data showing that European funds held $3 trillion worth of US equities in 2020, but this presence tripled by the end of last year to $9 trillion. He believes many of these European funds would prefer to be invested in European companies, suggesting a potential shift.

Matthew Fine: Referenced Michael Einhorn, who suggested that the “re-rating” dynamic common in past value investing might “never come back” due to a lack of new value investors being trained. However, Matt emphasized that simply by buying a business at 5.5 times earnings, one secures a 20% annual return to the owner, providing a great flow of returns without necessarily needing a re-rating. He stressed the importance of thinking like a business owner.

Christian Heck: Noted that private buyers are active and see the cheap companies. He spends time in Japan and the UK, finding many cheap businesses with various ways to profit.

Krishna Mohanraj: Agreed that re-rating shouldn’t be the core part of an investment thesis; it should merely be “icing on the cake.” They don’t depend on new shareholders entering the market.

Q: Tariffs & FX (Currency Risk)

The panel was asked about their approach to tariffs and currency fluctuations (FX).

Waldemar Mozes:

Tariffs: Many of their smaller portfolio companies already experienced financial disruptions from tariffs in 2017-2018. As a result, they have since been preparing, structuring supply chains, or finding alternative ways to mitigate damage from potential future tariffs.

FX: They do not hedge their currency exposure. The strengthening US dollar has been a 2% headwind for them over the last 7-9 years, largely due to capital flows into US assets. He believes this trend will eventually reverse, which would weaken the dollar.

Christian Heck:

Tariffs: The best way to insulate from tariffs is by having pricing power, which typically comes from scarcity – producing something people want with no substitutes. He believes most of First Eagle’s portfolio companies are well-insulated due to this inherent pricing power. He was not sure about FX.

Matthew Fine:

Tariffs: Even before tariffs, markets like copper were incredibly tight in terms of supply. When trade flows are disrupted and geopolitical trust breaks down, countries clamor for additional stockpiles, driving up prices and creating opportunities.

FX: He noted significant FX volatility in Japan last year, which created opportunities. He emphasized that just because a stock is denominated in a certain currency doesn’t mean that currency solely dictates its business exposure.

Amelia Koh:

Tariffs: Most of their companies sell locally, so they are not significantly impacted by tariffs. The primary issue is customer uncertainty, which can, in turn, create opportunities.

FX: One of Tweedy, Browne’s main funds is FX hedged, providing investors with a choice in how they manage currency exposure.